The End of Voluntary Recycling

The global energy transition has triggered an unprecedented expansion of battery energy storage systems to support renewable power generation, grid balancing and energy resilience. As deployment volumes continue to rise, the historical model of voluntary recycling commitments is giving way to legally binding end-of-life obligations. Extended Producer Responsibility (EPR) frameworks are becoming the dominant regulatory instrument, shifting financial and organizational responsibility for battery waste management directly onto producers.

For industrial BESS projects, a critical issue lies in how the term producer is defined in law. In several jurisdictions, liability does not remain with the original cell manufacturer. Instead, the entity that places the system on the market—often the system integrator or importer—assumes full responsibility for financing and organizing end-of-life treatment. This creates a long-tail liability that can extend decades beyond project commissioning and must be reflected in balance sheets, commercial contracts, and risk assessments.

The Global Compliance Divergence

The regulatory environment governing industrial-scale BESS recycling is no longer uniform. Instead, a clear compliance divergence has emerged across regions, complicating global project development, procurement, and asset-management strategies.

In the European Union, regulation is moving toward a data-centric circular economy model. Requirements such as battery passports, carbon footprint declarations, and detailed lifecycle data reporting are designed to ensure transparency from raw-material sourcing through end-of-life treatment. Compliance is becoming increasingly digital, auditable, and closely tied to market access.

The United States, by contrast, continues to prioritize safety, hazard mitigation, and fire-risk management. Circularity obligations remain fragmented at the state level, creating a patchwork of requirements rather than a unified national framework. The United Kingdom maintains a more traditional stewardship model that emphasizes physical take-back obligations, with more limited digital traceability requirements.

Outside Western markets, regulatory innovation is also accelerating. Taiwan applies an incentive-driven system that offers significant recycling fee discounts to encourage domestic treatment, while Australia is moving toward mandatory stewardship supported by eco-modulated levies. For multinational system integrators, navigating these diverging approaches has become an operational and financial challenge rather than a purely legal one.

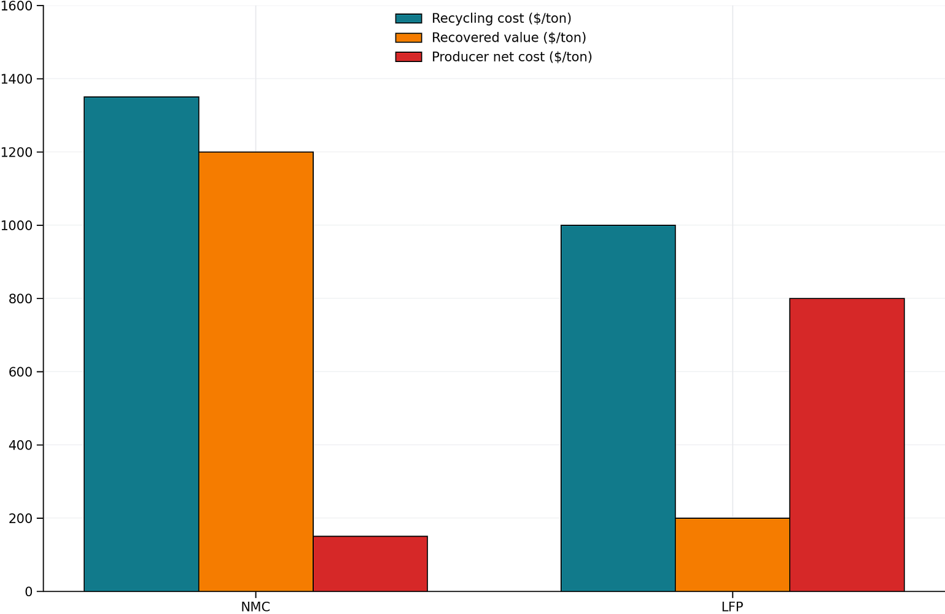

The LFP Paradox and the “Net Cost” Problem

Lithium-iron phosphate chemistry has emerged as the dominant choice for utility-scale energy storage because of its thermal stability, long cycle life, and comparatively low upfront cost. However, from an end-of-life perspective, LFP presents a structural economic disadvantage.

Unlike nickel- or cobalt-rich chemistries, LFP batteries contain only limited quantities of high-value recoverable materials. As a result, revenues generated from material recovery rarely cover the costs of collection, transportation, and advanced recycling. Under EPR frameworks such as the European Union’s “net cost” principle, producers are financially responsible for covering this gap.

In practice, this means that current EPR regulation functions as a persistent financial penalty on LFP-based systems. Even when recycling targets are met, producers face predictable and recurring costs that must be provisioned over the full lifecycle of the asset. What was once viewed as a sustainability concern has therefore become a permanent line item in long-term financial planning.

The Second-Life Grey Area

As industrial BESS installations approach the end of their primary grid-service life, second-life applications, such as stationary backup power or lower-demand energy storage, offer a potential way to offset recycling costs. Repurposing can extend asset value and delay material processing, transforming a disposal obligation into a secondary revenue stream.

However, second-life deployment introduces a regulatory grey area concerning the transfer of EPR liability. In many jurisdictions, it remains unclear at what point responsibility shifts from the original producer to a secondary-market operator. Without standardized legal frameworks governing this handover, original producers risk retaining end-of-life liabilities for assets they no longer control.

This uncertainty complicates contractual arrangements and discourages large-scale second-life investment, particularly for risk-averse asset owners. Until liability-transfer mechanisms are clarified, second-life strategies must be approached with caution and supported by robust legal, technical, and insurance frameworks.

Bridging the Gap: The Transition to Compliance-as-a-Service

To manage growing regulatory complexity, system integrators are increasingly required to evolve beyond traditional equipment-supply models. A shift toward lifecycle-oriented partnerships is emerging, often described as Compliance-as-a-Service (CaaS).

Under this model, environmental liabilities are embedded directly into long-term service agreements. Digital data hosting, regulatory reporting, physical recycling logistics, and the formal assumption of EPR obligations are consolidated into a single contractual offering. For asset owners, this approach converts uncertain regulatory exposure into a predictable service cost.

From a competitive perspective, CaaS offers a powerful differentiator. By neutralizing regulatory risk, system integrators can strengthen customer relationships, support project bankability, and align compliance management with long-term operational performance. In an environment where regulation is tightening faster than technology costs are falling, compliance capability is becoming nearly as critical as system efficiency itself.